The aerospace and defence industry continues to be a hotbed of innovation, with the conflict in Ukraine driving defence spending and investment, the need to combat emerging technologies such as hypersonics, and growing importance of technologies such as AI and computer vision. In the last three years alone, there have been over 174,000 patents filed and granted in the aerospace and defence industry, according to GlobalData’s report on Robotics in Aerospace, Defence & Security: Machine learning for autonomous navigation. Buy the report here.

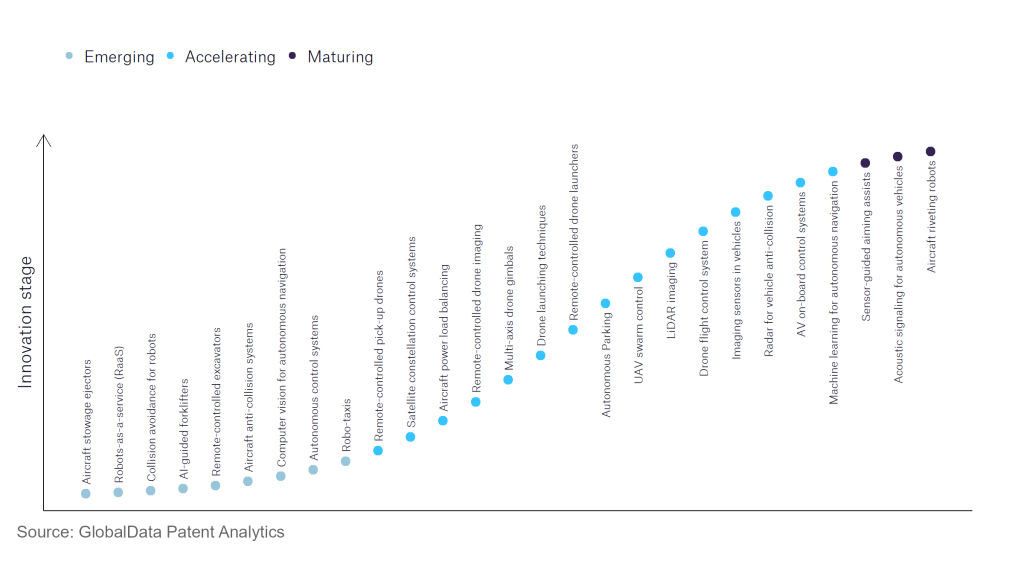

However, not all innovations are equal and nor do they follow a constant upward trend. Instead, their evolution takes the form of an S-shaped curve that reflects their typical lifecycle from early emergence to accelerating adoption, before finally stabilising and reaching maturity.

Identifying where a particular innovation is on this journey, especially those that are in the emerging and accelerating stages, is essential for understanding their current level of adoption and the likely future trajectory and impact they will have.

180+ innovations will shape the aerospace and defence industry

According to GlobalData’s Technology Foresights, which plots the S-curve for the aerospace and defence industry using innovation intensity models built on over 262,000 patents, there are 180+ innovation areas that will shape the future of the industry.

Within the emerging innovation stage, collision avoidance for robots, computer vision for autonomous navigation, and autonomous control systems are disruptive technologies that are in the early stages of application and should be tracked closely. UAV swarm control, and drone flight control system are some of the accelerating innovation areas, where adoption has been steadily increasing. Among maturing innovation areas are sensor-guided aiming assists which are now well established in the industry.

Innovation S-curve for robotics in the aerospace and defence industry

Machine learning for autonomous navigation is a key innovation area in robotics

Autonomous navigation describes the ability of a vehicle to execute movement along a path without human intervention or oversight. The technology is built on neural networks and operates through cameras, sensors and radars.

GlobalData’s analysis also uncovers the companies at the forefront of each innovation area and assesses the potential reach and impact of their patenting activity across different applications and geographies. According to GlobalData, there are 40+ companies, spanning technology vendors, established aerospace and defence companies, and up-and-coming start-ups engaged in the development and application of machine learning for autonomous navigation.

Key players in machine learning for autonomous navigation – a disruptive innovation in the aerospace and defence industry

‘Application diversity’ measures the number of different applications identified for each relevant patent and broadly splits companies into either ‘niche’ or ‘diversified’ innovators.

‘Geographic reach’ refers to the number of different countries each relevant patent is registered in and reflects the breadth of geographic application intended, ranging from ‘global’ to ‘local’.

Patent volumes related to machine learning for autonomous navigation

Source: GlobalData Patent Analytics

The largest patent filer in this sector is Stradvision, which has invested significantly in autonomous capabilities and driver assistance systems. The company provides solutions for machine learning which reduces the need for human intervention and can detect roadside objects including traffic signs, parking spaces etc. Intel is the second largest company in the sector and has developed machine learning for a variety of capabilities including robots, drones and intelligent machines. Intel’s aim is to support the development of autonomous systems which can make independent decisions with no or minimal human oversight.

Cognata has the most application diversity, producing capabilities for commercial and military use and enabling off-road capabilities utilising a variety of cameras and modelling technology. The second biggest company in terms of application diversity is Chongqing Jinkang New Energy Vehicle, a Chinese electric vehicle maker which aims to manufacture smart EVs. PlusAI is the largest company in terms of geographic reach, with Stradvision in second place and Volta Robots in third.

The number of patents in this sector indicates ongoing growth, with a number of companies investing in modelling technology in order to develop the technology before deployment in the real world.

To further understand the key themes and technologies disrupting the aerospace and defence industry, access GlobalData’s latest thematic research report on Defence.

Data Insights

From

![]()

The gold standard of business intelligence.

Blending expert knowledge with cutting-edge technology, GlobalData’s unrivalled proprietary data will enable you to decode what’s happening in your market. You can make better informed decisions and gain a future-proof advantage over your competitors.

GlobalData, the leading provider of industry intelligence, provided the underlying data, research, and analysis used to produce this article.

GlobalData’s Patent Analytics tracks patent filings and grants from official offices around the world. Textual analysis and official patent classifications are used to group patents into key thematic areas and link them to specific companies across the world’s largest industries.